Mortgage rates today are higher than they were three months ago. While it is not entirely clear why rates have risen so much in the first quarter of the year, it is possible that they will continue to rise in the second. Interest rates are determined by a combination of factors that are both market-based and specific to you. This article discusses the factors that affect mortgage rates today. In addition to a host of market-specific factors, the following factors may influence mortgage rates in your area.

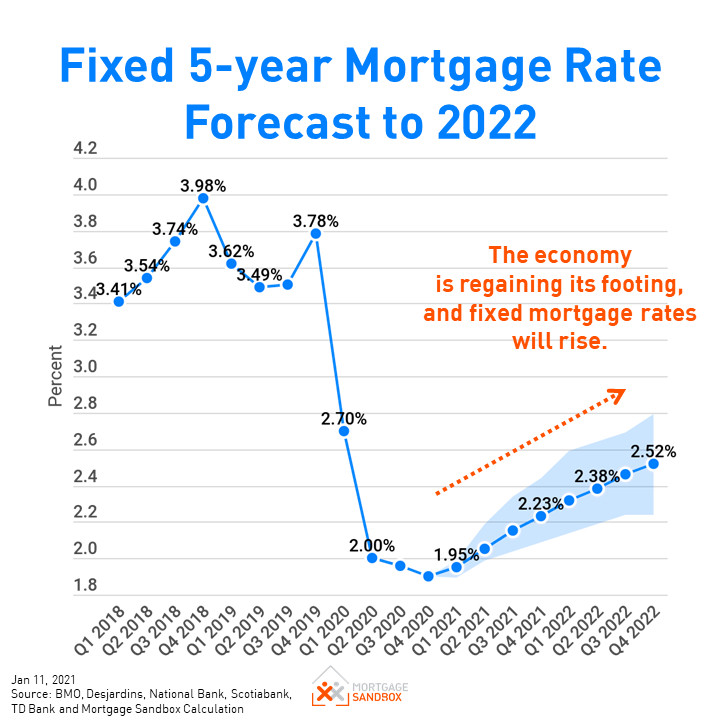

Interest rates on mortgages increased in the first three months of the year

While the Federal Reserve does not set mortgage interest rates, they typically follow 10-year US Treasury bonds. As a result, Fed action on inflation expectations indirectly affects mortgage rates. For instance, when the Fed expects that prices will increase, investors tend to sell government bonds, sending yields higher. In turn, higher yields affect mortgage rates. Last week, the Fed raised its benchmark interest rate by 75 basis points, which dampened demand for housing.

Mortgage rates have been near record lows this year – the average 30-year fixed-rate mortgage was at a historic low of 2.65% a year ago. Although the increase won’t derail the highly competitive U.S. housing market, it will affect the purchasing power of would-be homeowners. Furthermore, homeowners considering refinancing may miss the opportunity to lock in a lower rate if interest rates increase in the coming months.

Mortgage rates are likely to continue to rise for the rest of the year. The steepest hikes will likely affect the largest part of the market. Mortgage rates can increase by over seven percent. However, they may bottom out at about this point or continue rising further. Until such a time, it is important to compare mortgage rates from multiple lenders. If you’re looking to buy a house, consider refinancing.

While mortgage rates are expected to increase for the rest of the year, many economists predict that the average rate on a 30-year fixed-rate mortgage will rise by a full five percent this year. A few economists still predict that rates will continue to rise, but a slowdown is coming. With rising these rates, many would-be homebuyers may be pushed out of the market.

The rates on mortgages are constantly fluctuating. They follow the federal funds rate, which is the amount banks pay to borrow money. Other factors that affect mortgage rates include inflation, the bond market, and the overall condition of the housing market. Mortgage rates tend to rise and fall with the overall shape of the housing market. However, they are currently lower than they were last year. In addition, mortgage rates are now below 4%.

They may raise more in the second

According to experts, Second home mortgage rates are set to rise this year. While the increase won’t happen overnight and won’t be dramatic, mortgage rates will be near their historically low levels for most of the first half of the year. Later in the year, mortgage rates will likely rise more, but for now, the low rates are still favorable for buying a new home or refinancing your existing mortgage.

In addition to macroeconomic factors, these rates are affected by industry and bond market movements. The yield on 10-year Treasury notes fell below one percent in March 2020, but it has been rising ever since. There’s an average spread between Treasury yields and benchmark mortgage rates of 1.8 points. With so much at stake, it’s no wonder that these rates may rise more in the second half of the year.

If the Fed decides to increase its benchmark interest rate by 75 basis points this year, that would be the largest increase since 1994. With the Fed preparing to raise rates again this year, many economists expect interest rates to increase even higher. Whether mortgage rates rise more this year or not depends on how the virus develops. Either way, it’s critical for consumers to act quickly to organize their debt and lock in their mortgage rates now.

If the predictions for mortgage rates in May are accurate, the collective doubt about home purchasing will likely snowball. According to the National Association of Realtors (NAR), the average interest rate on 30-year fixed-rate mortgages will increase by 5.2 percent this month. That’s double the rate they were at last year. With more home buyers delaying a purchase until rates fall.

The MBA and other industry experts predict that mortgage interest rates will level off over the next few years. But it’s hard to predict stability, but historical data suggests that rates rise and fall for a while. However, if these rates remain high, home buying may become harder for entry-level homebuyers. Ultimately, the mortgage market will have to adapt to a rising rate environment to remain competitive.

They are influenced by a mix of factors that are specific to you

The overall economy plays a role in mortgage rates today, but you may not be aware of these factors. Home sales and GDP both affect mortgage rates and rising or declining home sales will affect your rate, too. If your home sales are down, these rates may fall, but if they’re up, they will likely go up. When home sales are down, the opposite will happen.

Along with the economy, the economy’s financial health will affect interest rates. That’s What You’re Paying on Your Mortgage. Several factors determine the rate you charge. That includes your down payment and equity amount.. Your credit score is one factor that indicates how much risk you’re willing to assume. These factors, although initially confusing, affect the interest rate you pay.

In addition to the economy, the stock market also affects interest rates. While treasury yield rates don’t predict mortgage rates, they tend to rise faster when treasury rates are low and fall more slowly when rates are high. Moreover, these rates tend to increase during periods of high inflation, while decreasing prices mean the opposite. While you can’t predict what the stock market will do, the stock market can tell you how much confidence investors have in the economy.

They are influenced by non-market forces

There are a number of factors that influence mortgage rates today, including the general economy. Higher GDP and higher employment mean that the economy is growing and the demand for goods and services is high. Increasing interest rates are one way to reduce this rising demand. However, when the economy is stagnant or slowing down, these rates tend to decline, as they are less profitable. The Federal Reserve has a vested interest in reducing inflation and rising interest rates in order to slow the economy.

In addition to the stock market, unexpected events can cause these rates to rise or fall. Unpredicted events such as the COVID-19 pandemic, a severe weather event, or a natural disaster can lead to panic in the markets. This can cause money to move to safe investments and mortgage bonds pick up on the momentum of panicked investors. Recent natural disasters, such as earthquakes and tsunamis, have also been credited with pushing these rates down.

While the monetary policy of the Federal Reserve influences these rates, the conditions of the housing market are also a major factor. A strong economy means more demand for mortgages. If the housing market is not strong enough, the interest rate for mortgages will fall. Conversely, if the housing market is poor, the monetary policy of the Federal Reserve puts downward pressure on interest rates. However, when the housing market is strong, these rates tend to increase.

In addition to the monetary policy, personal factors can also influence the interest rate. Lenders evaluate these factors to determine the risk level of a loan. Generally, borrowers with better qualifying factors are likely to receive higher interest rates. Other non-market factors influence these rates, such as the general economy. When the economy is doing well, mortgage rates tend to increase and when it is not, mortgage rates typically fall.